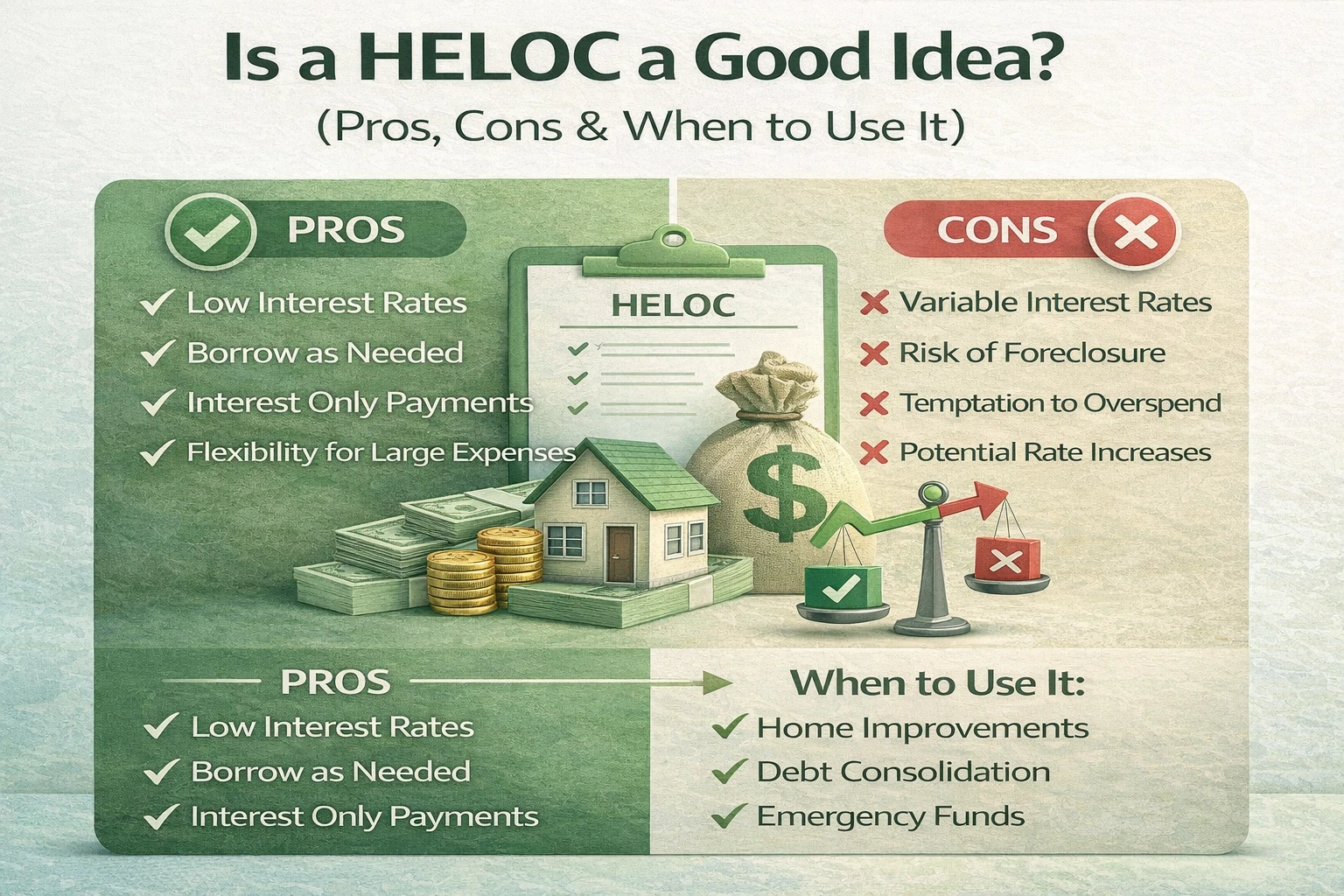

✅ Pros of a HELOC

Lower Interest Rates Than Credit Cards

HELOCs typically offer rates of 6-10%, compared to 18-25% for credit cards. This can save thousands in interest.

Flexible Borrowing

Borrow only what you need, when you need it. Pay interest only on the amount you use, not your entire credit limit.

Large Credit Limits

Access up to 80-90% of your home equity, often $50,000 to $500,000 or more depending on your home value.

Tax-Deductible Interest (Sometimes)

Interest may be tax-deductible if used for home improvements. Consult a tax professional for your situation.

Interest-Only Payments During Draw

Lower monthly payments during the draw period (typically 5-10 years) give you financial flexibility.

❌ Cons of a HELOC

Variable Rates

Your interest rate can increase, causing your monthly payment to rise unexpectedly. Rate increases can double your payment.

Risk of Foreclosure

Your home secures the HELOC. If you can't make payments, you could lose your house.

Payments Can Increase

When you enter the repayment period, payments can double or triple as you begin paying principal plus interest.

Temptation to Overspend

Easy access to large amounts of money can lead to unnecessary spending and increased debt.

Closing Costs & Fees

Application fees, appraisal costs, and annual fees can add $500-$5,000 to your total cost.

📊 When a HELOC Makes Sense

- ✓ You have strong equity – At least 20% equity in your home

- ✓ Stable income – Consistent earnings to handle payments

- ✓ Clear repayment plan – Know how you'll pay it back

- ✓ Home improvements – Projects that increase home value

- ✓ Emergency fund backup – Safety net for unexpected expenses

- ✓ Good credit score – 700+ to qualify for best rates

⚠️ When to Avoid a HELOC

- ✗ Unstable income – Job insecurity or irregular earnings

- ✗ High debt levels – Already struggling with existing debt

- ✗ Risky investments – Using borrowed money for speculative ventures

- ✗ Discretionary spending – Vacations, luxury items, or lifestyle inflation

- ✗ Near retirement – Limited time to repay before income drops

- ✗ Planning to sell soon – Must pay off HELOC when selling

💡 Best Uses for a HELOC

Home Improvements

Kitchen remodels, bathroom upgrades, or additions that increase home value.

ROI: Often 60-80% of investment

Debt Consolidation

Pay off high-interest credit cards or personal loans.

Savings: Can cut interest by 50-70%

Emergency Fund

Backup for unexpected medical bills or major repairs.

Benefit: Only pay interest when used

Education Expenses

College tuition when rates are lower than student loans.

Compare: HELOC vs federal student loans

🚫 Worst Uses for a HELOC

Vacations & Luxury Items

Never risk your home for discretionary spending. Use savings instead.

Speculative Investments

Stock market, crypto, or risky ventures. If the investment fails, you still owe the debt.

Daily Living Expenses

Using a HELOC to cover regular bills indicates deeper financial problems that need addressing.

Depreciating Assets

Cars, boats, or electronics lose value quickly. Don't secure them with your home.

🎯 Decision Framework

Ask Yourself These Questions:

- Can I afford the payments if rates increase by 2-3%?

- Do I have a clear plan to repay the borrowed amount?

- Will this expense increase my home value or financial position?

- Do I have stable income for the next 5-10 years?

- Am I comfortable with variable payments?

If you answered "no" to any of these, reconsider getting a HELOC.

❓ Frequently Asked Questions

Is a HELOC better than a personal loan?

Often yes, due to lower interest rates. However, personal loans don't risk your home and have fixed payments, making them safer for some situations.

Can a HELOC hurt my credit score?

Opening a HELOC may temporarily lower your score due to the hard inquiry and increased debt. However, responsible use can improve your credit over time.

What if I never use my HELOC?

You typically don't pay interest on unused funds. Some lenders charge annual fees ($50-$100), but many have no fees if unused.

Should I get a HELOC as an emergency fund?

It can serve as a backup, but don't rely on it as your only emergency fund. Keep 3-6 months of expenses in savings first.

Is now a good time to get a HELOC?

It depends on current interest rates and your personal situation. Compare rates from multiple lenders and consider if you can handle potential rate increases.