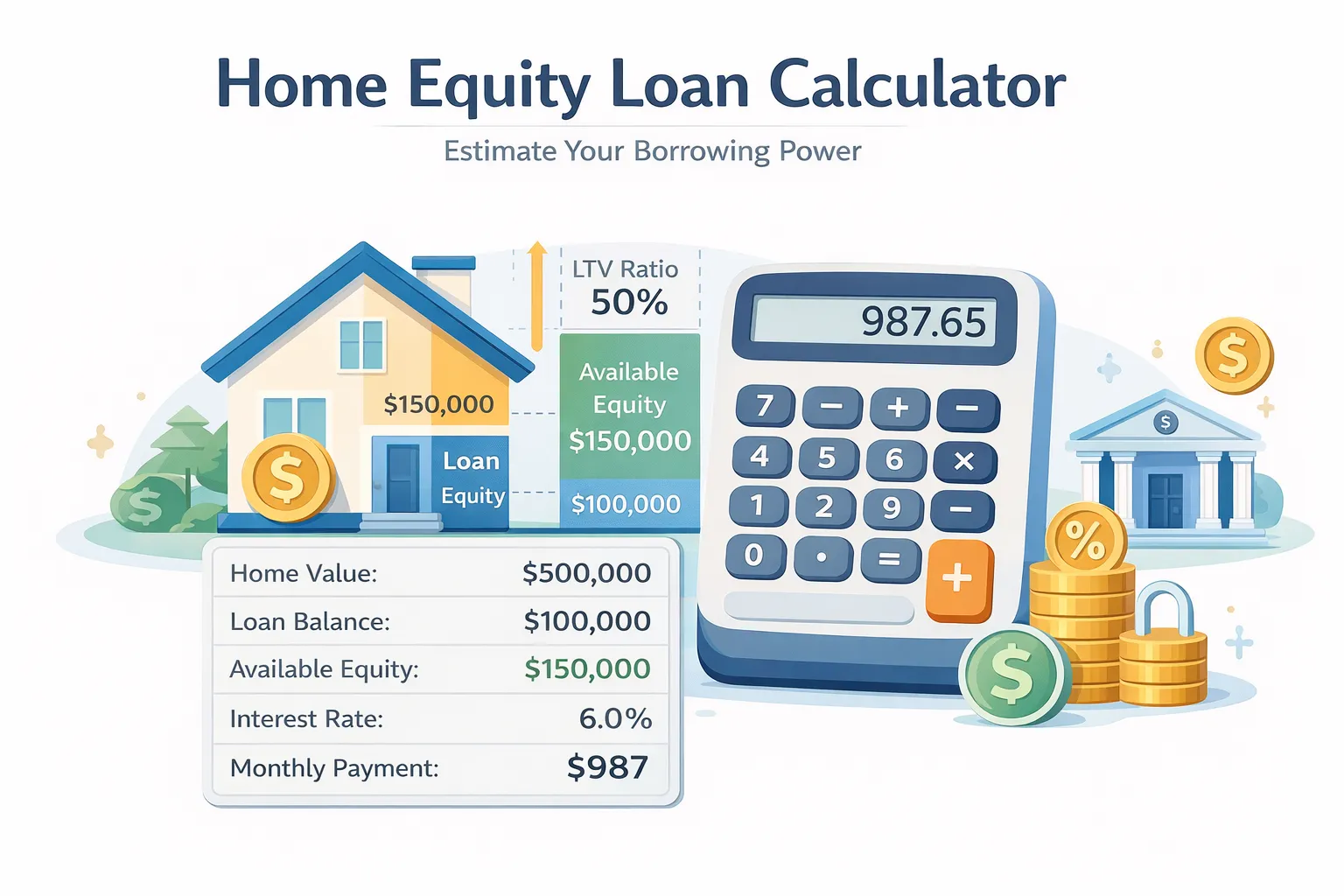

What Is a Home Equity Loan Calculator?

A home equity loan calculator is a financial tool that helps you estimate monthly payments, total interest costs, and borrowing capacity based on your home's value and existing mortgage balance. This free home equity loan payment calculator uses standard amortization formulas to provide accurate projections for fixed-rate home equity loans.

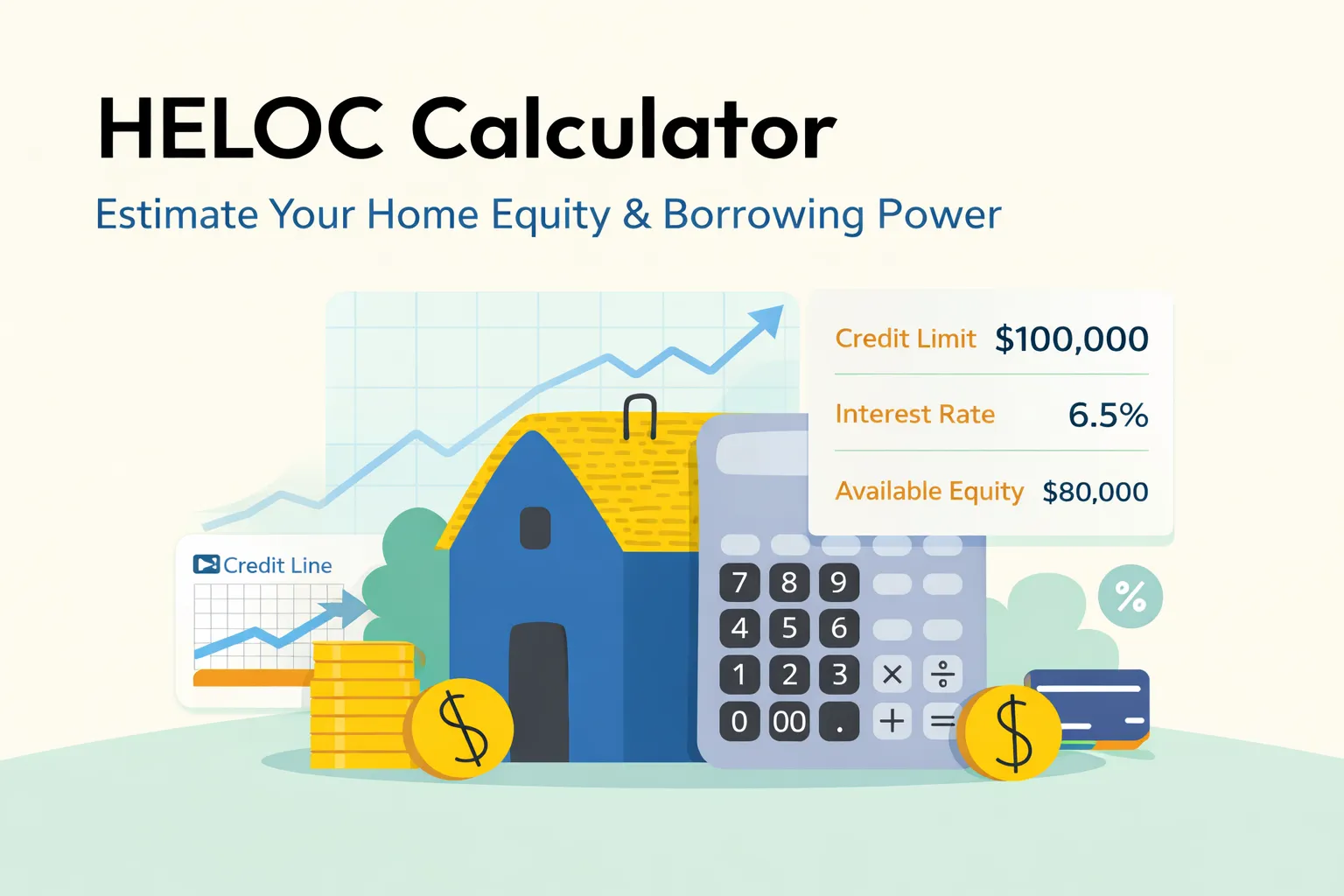

Unlike a HELOC calculator which handles revolving credit lines with variable rates, this calculator focuses on traditional home equity loans with lump-sum disbursement and fixed monthly payments throughout the loan term.

What It Calculates

- Monthly Payment - Your fixed payment amount for principal and interest

- Total Interest - How much interest you'll pay over the life of the loan

- Borrowing Limit - Maximum amount you can borrow based on your home equity

- LTV Ratio - Loan-to-value ratio to assess lending risk

- Amortization Schedule - Month-by-month breakdown of payments

How Does a Home Equity Loan Calculator Work?

This home equity loan payment calculator uses the standard amortization formula to calculate your fixed monthly payment. The formula accounts for your loan amount, interest rate, and loan term to determine exactly how much you'll pay each month.

Key Inputs

- Home Value: Current market value of your property

- Mortgage Balance: Outstanding balance on your primary mortgage

- Loan Amount: How much you want to borrow

- Interest Rate: Annual percentage rate (typically 7-10% in 2026)

- Loan Term: Repayment period (usually 5-30 years)

The Formula

The monthly payment formula for a home equity loan is:

Where: M = Monthly payment, P = Loan amount, r = Monthly interest rate, n = Number of payments

Home Equity Loan Payment Calculator: Step-by-Step Guide

Follow these steps to calculate your home equity loan payment accurately:

- Enter your home value - Use a recent appraisal or online estimate

- Input your mortgage balance - Check your latest mortgage statement

- Specify desired loan amount - How much you need to borrow

- Enter the interest rate - Get quotes from multiple lenders

- Select loan term - Choose between 5-30 years

- Click calculate - Get instant results with payment breakdown

Pro Tip:

Use the preset scenarios above to quickly compare different loan amounts and terms. Even small changes in interest rate or term length can significantly impact your total cost.

How Much Can You Borrow? Home Equity Calculator

Most lenders allow you to borrow up to 80-85% of your home's value minus your existing mortgage balance. This is called the loan-to-value (LTV) ratio, and it's a key factor in determining your borrowing power.

LTV Formula Explained

Step 1: Calculate maximum loan amount

Maximum = Home Value × LTV Ratio (typically 80%)

Step 2: Subtract existing mortgage

Available Equity = Maximum - Mortgage Balance

Example Calculation

Scenario:

- 🏠 Home Value: $600,000

- 💰 Mortgage Balance: $250,000

- 📊 LTV Ratio: 80%

Calculation:

Maximum Loan: $600,000 × 0.80 = $480,000

Available Equity: $480,000 - $250,000 = $230,000

✅ You can borrow up to $230,000

Home Equity Loan Rates Today (2026)

Home equity loan rates in 2026 typically range from 7% to 10%, depending on various factors. These rates are generally 1-2 percentage points higher than primary mortgage rates but lower than credit card rates, making them attractive for debt consolidation and large purchases.

What Affects Your Rate

📊 Credit Score

700+: Best rates (7-8%)

680-699: Good rates (8-9%)

620-679: Higher rates (9-10%)

💰 Debt-to-Income Ratio

Lower DTI = better rates. Lenders prefer DTI below 43% including the new loan payment.

📈 LTV Ratio

Lower LTV = lower risk = better rates. Keep LTV under 80% for best terms.

🌐 Market Conditions

Federal Reserve policy and economic conditions influence all lending rates.

Costs of a Home Equity Loan

Beyond the monthly payment, home equity loans come with upfront and ongoing costs that can add 2-5% to your total borrowing expense.

Upfront Costs

| Cost Type | Typical Range | Description |

|---|---|---|

| Appraisal Fee | $300 - $500 | Required to determine home value |

| Origination Fee | 0.5% - 1% of loan | Lender processing fee |

| Title Search | $200 - $400 | Verify property ownership |

| Recording Fees | $50 - $250 | Government filing fees |

| Total Closing Costs | 2% - 5% of loan | All fees combined |

Ongoing Costs

- Monthly Interest: Included in your fixed payment

- Property Insurance: May need to increase coverage

- Property Taxes: Remain your responsibility

Home Equity Loan vs HELOC: Which Is Better?

Both tap into your home equity, but they work very differently. Here's a comprehensive comparison to help you choose:

| Feature | Home Equity Loan | HELOC |

|---|---|---|

| Structure | Lump sum ✓ | Revolving credit line |

| Interest Rate | Fixed ✓ | Variable |

| Payment | Fixed P+I ✓ | Interest-only then P+I |

| Flexibility | Low - one-time funding | High - borrow as needed ✓ |

| Best For | One-time large expense | Ongoing expenses |

| Rate Risk | None - rate locked ✓ | Higher - rates can increase ⚠️ |

Choose a Home Equity Loan if: You need a specific amount for a one-time expense (home renovation, debt consolidation), want payment certainty, and prefer fixed rates.

Choose a HELOC if: You have ongoing expenses, want flexibility to borrow and repay multiple times, or expect to pay off quickly. Use our HELOC calculator to compare.

Best Ways to Use a Home Equity Loan

Home equity loans work best for value-adding purposes that justify the risk of using your home as collateral:

✅ Smart Uses

- 🏠 Home Improvements: Adds value to your property

- 💳 Debt Consolidation: Lower rate than credit cards

- 🎓 Education: Investment in earning potential

- 🏥 Medical Expenses: Necessary large costs

- 💼 Business Investment: Revenue-generating purposes

❌ Avoid Using For

- ✈️ Vacations: Depreciating expense

- 🚗 Vehicles: Depreciate faster than loan payoff

- 🛒 Daily Expenses: Sign of budget problems

- 📉 Risky Investments: Could lose home and investment

- 💎 Luxury Items: Not worth the risk

Golden Rule:

Only borrow against your home for expenses that either increase your home's value, reduce higher-interest debt, or generate future income. Your home is your largest asset - protect it wisely.

Risks & Considerations

While home equity loans offer attractive rates and tax benefits, they come with significant risks you must understand:

Risk of Foreclosure

Your home is collateral. If you can't make payments, the lender can foreclose and you'll lose your home. This is the most serious risk and why you should only borrow what you can comfortably afford to repay.

Overborrowing

Just because you can borrow up to 80% LTV doesn't mean you should. Leave equity cushion for:

- Market downturns (home values can decrease)

- Emergency expenses

- Future refinancing options

- Selling flexibility (avoid being underwater)

Market Fluctuations

If home values drop significantly, you could owe more than your home is worth. This happened to millions during the 2008 financial crisis. Maintain at least 20% equity cushion to protect against market volatility.

⚠️ Before You Borrow, Ask Yourself:

- ❓ Can I afford the payment if I lose my job?

- ❓ Will this expense add value or generate income?

- ❓ Have I shopped for the best rate?

- ❓ Do I have an emergency fund?

- ❓ Am I comfortable with the total interest cost?

Home Equity Loan Payment Calculation Formula

Home equity loans use standard amortization formulas for fixed monthly payments:

- Available Equity = (Home Value × LTV Ratio) - Mortgage Balance

- Monthly Payment = P × [r(1+r)^n] ÷ [(1+r)^n - 1]

- P = Loan Amount

- r = Monthly Interest Rate (Annual Rate ÷ 12)

- n = Total Number of Payments (Years × 12)

- Total Interest = (Monthly Payment × n) - P

Example: Home Equity Loan Calculation

Calculate monthly payment for a typical home equity loan:

Frequently Asked Questions

How do you calculate a home equity loan payment?

Use the amortization formula: M = P × [r(1+r)^n] ÷ [(1+r)^n - 1], where P is the loan amount, r is the monthly interest rate, and n is the number of payments. For a $150,000 loan at 8% for 15 years, the monthly payment is $1,433.48. This calculator automates the process for accurate results.

How much home equity can I borrow?

Most lenders allow you to borrow up to 80-85% of your home's value minus your mortgage balance. For example, with a $600,000 home and $250,000 mortgage, you could borrow up to $230,000 (80% LTV). Your actual borrowing limit depends on credit score, income, and lender requirements.

What credit score is needed for a home equity loan?

Most lenders require a minimum credit score of 620-680 for home equity loans. Better rates typically require 700+. Higher credit scores qualify for lower interest rates, potentially saving thousands over the loan term. Check your credit before applying.

Are home equity loans risky?

Yes, home equity loans use your home as collateral. If you can't make payments, you risk foreclosure. Only borrow what you can afford to repay, and use funds for value-adding purposes like home improvements or debt consolidation, not depreciating assets.

What are current home equity loan rates in 2026?

Home equity loan rates in 2026 typically range from 7-10% depending on credit score, loan amount, and lender. Rates are generally 1-2% higher than primary mortgage rates. Shop multiple lenders to find the best rate for your situation.

What's the difference between a home equity loan and HELOC?

A home equity loan provides a lump sum with fixed rates and fixed payments. A HELOC is a revolving credit line with variable rates and flexible payments. Home equity loans are better for one-time expenses, while HELOCs suit ongoing costs.

How long does it take to get a home equity loan?

Home equity loans typically take 2-6 weeks from application to closing. The process includes application, appraisal, underwriting, and closing. Having documents ready (income verification, tax returns, insurance) can speed up approval.

What are the closing costs for a home equity loan?

Closing costs typically range from 2-5% of the loan amount ($3,000-$7,500 on a $150,000 loan). Costs include appraisal ($300-$500), origination fees (0.5-1%), title search, and recording fees. Some lenders offer no-closing-cost options with slightly higher rates.

Can I pay off a home equity loan early?

Most home equity loans allow early payoff without penalties, but check your loan agreement. Paying extra toward principal reduces total interest and shortens the loan term. Even small extra payments can save thousands in interest.

Related Calculators

Explore more tools to help with your calculations

HELOC Calculator 2026 | Free Payment Estimates

Calculate HELOC payments, interest costs, and payoff timeline. Free HELOC calculator with interest-only and amortization schedules for home equity lines of credit.

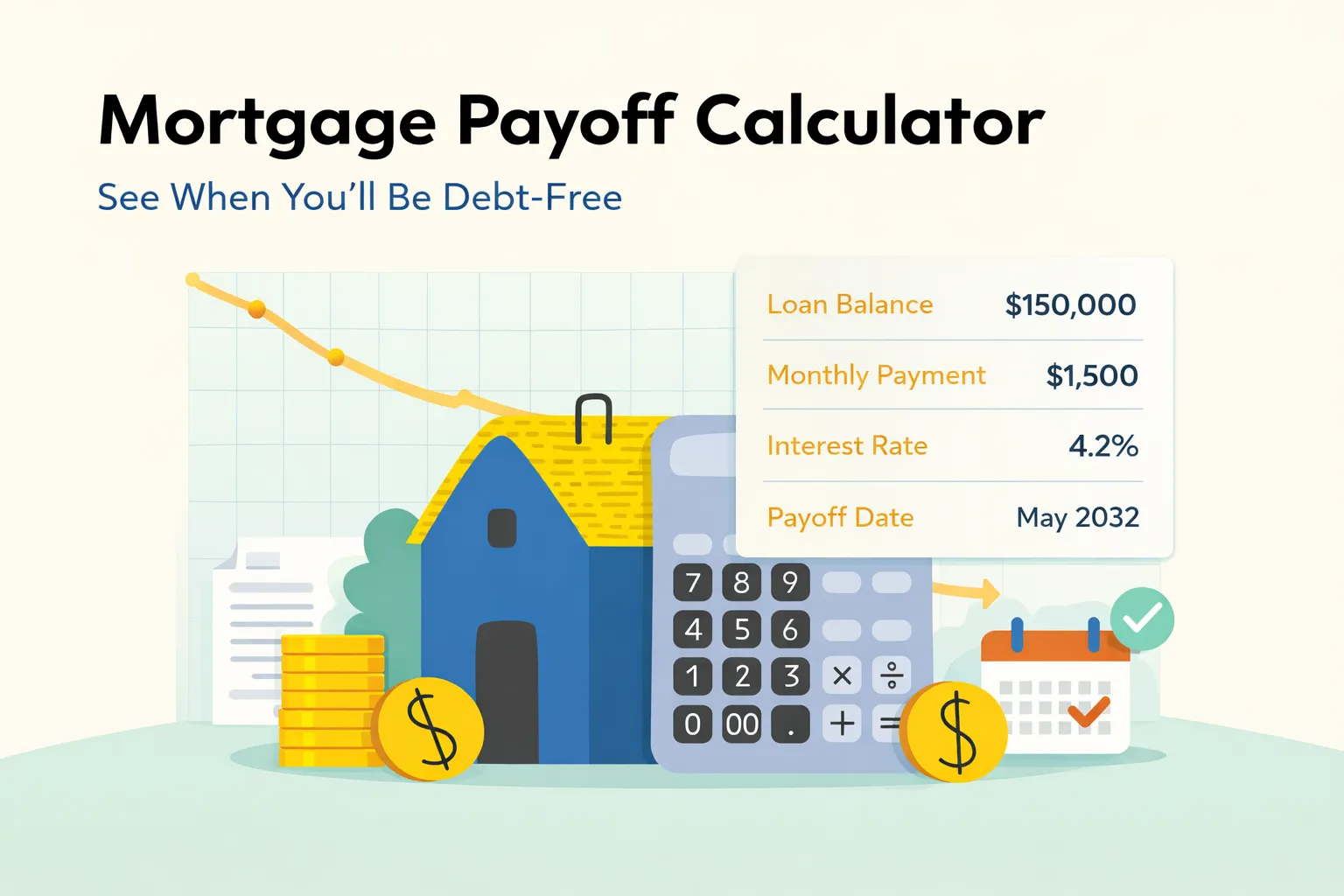

Mortgage Payoff Calculator 2026 | Save $50K+ Fast

Calculate how much you can save by making extra mortgage payments and when you'll pay off your loan.

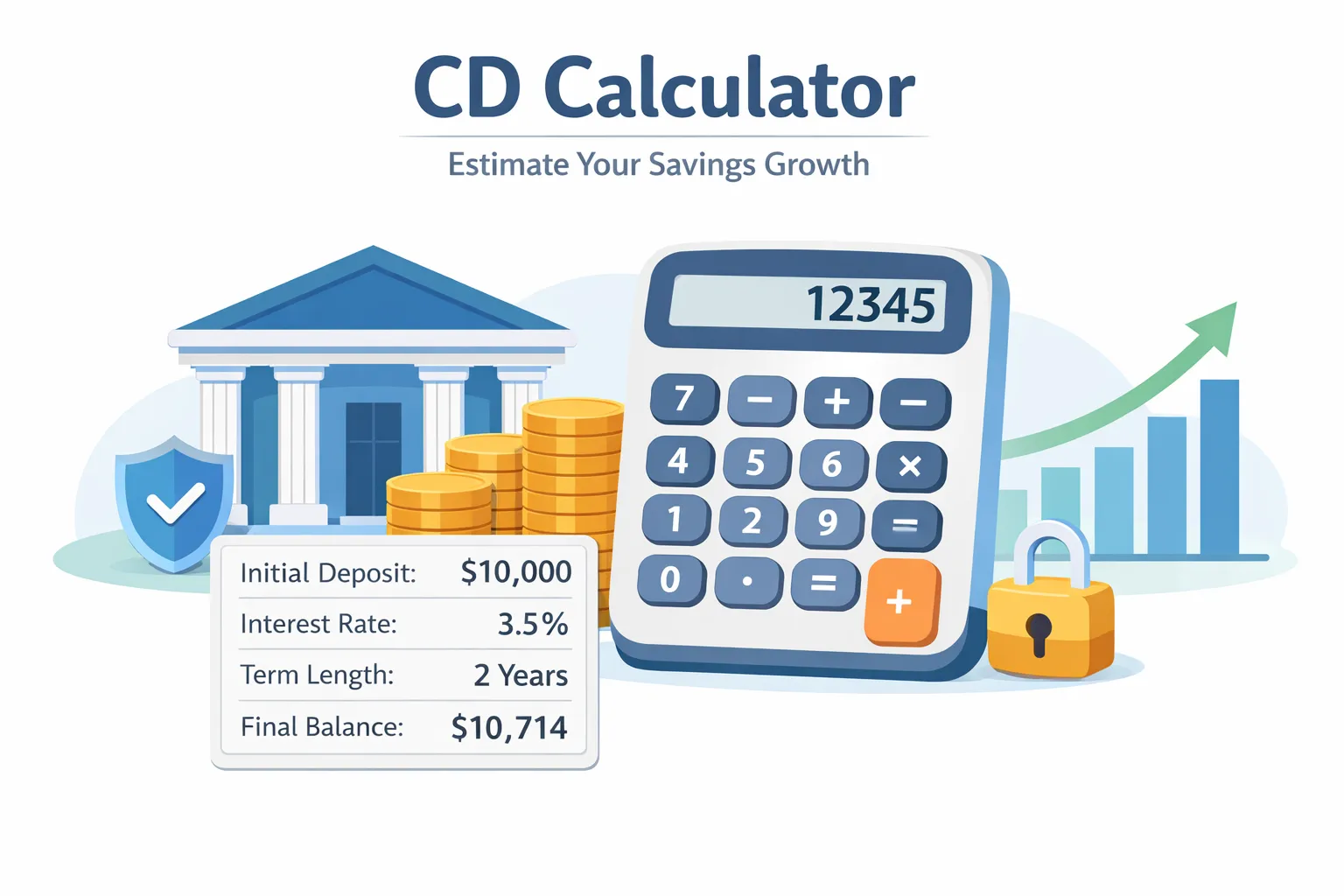

CD Calculator 2026 | Maximize Your Returns Now

Use a CD calculator to estimate your earnings, compare CD rates, and maximize returns in 2026. Includes formulas, examples, and expert strategies.