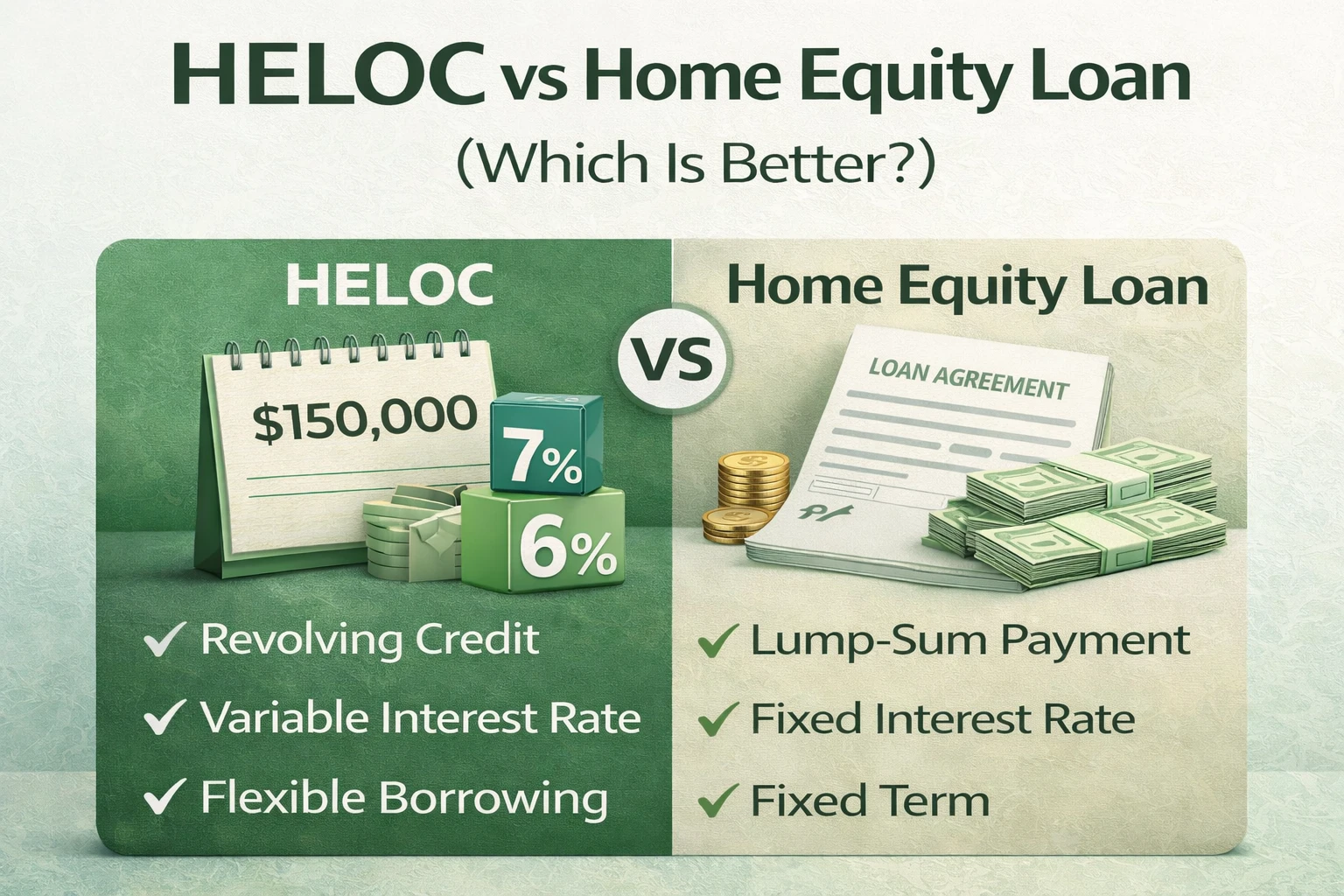

📊 Key Differences

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Type | Credit line | Lump sum |

| Rate | Variable | Fixed |

| Flexibility | High | Low |

| Payment | Variable | Predictable |

| Best For | Ongoing expenses | One-time expense |

🏠 When to Choose HELOC

- • Ongoing expenses – Home renovations done in phases

- • Renovation projects – Draw funds as needed during construction

- • Flexible borrowing – Emergency fund or multiple expenses

- • Lower initial payments – Interest-only during draw period

🏠 When to Choose Home Equity Loan

- • One-time expense – Debt consolidation or single purchase

- • Fixed payment preference – Want predictable monthly costs

- • Lower risk tolerance – Avoid variable rate uncertainty

- • Budget planning – Need consistent payment amounts

⚠️ Risks

HELOC Risks

- • Rate increases can double payments

- • Temptation to overborrow

- • Payment shock during repayment phase

Home Equity Loan Risks

- • Less flexibility if needs change

- • May pay interest on unused funds

- • Refinancing costs if you need more

❓ Frequently Asked Questions

Which is cheaper?

It depends on interest rates and how you use the funds. HELOCs often start cheaper but can become more expensive if rates rise.

Can I have both?

Yes, you can have both a HELOC and a home equity loan simultaneously, as long as your combined LTV stays within lender limits (typically 80-90%).

Which is easier to qualify for?

Requirements are similar for both. HELOCs may have slightly stricter credit requirements due to the variable rate risk.

Can I convert a HELOC to a home equity loan?

Some lenders allow you to convert all or part of your HELOC balance to a fixed-rate loan, giving you payment stability.