What Is a CD Calculator and Why It Matters in 2026

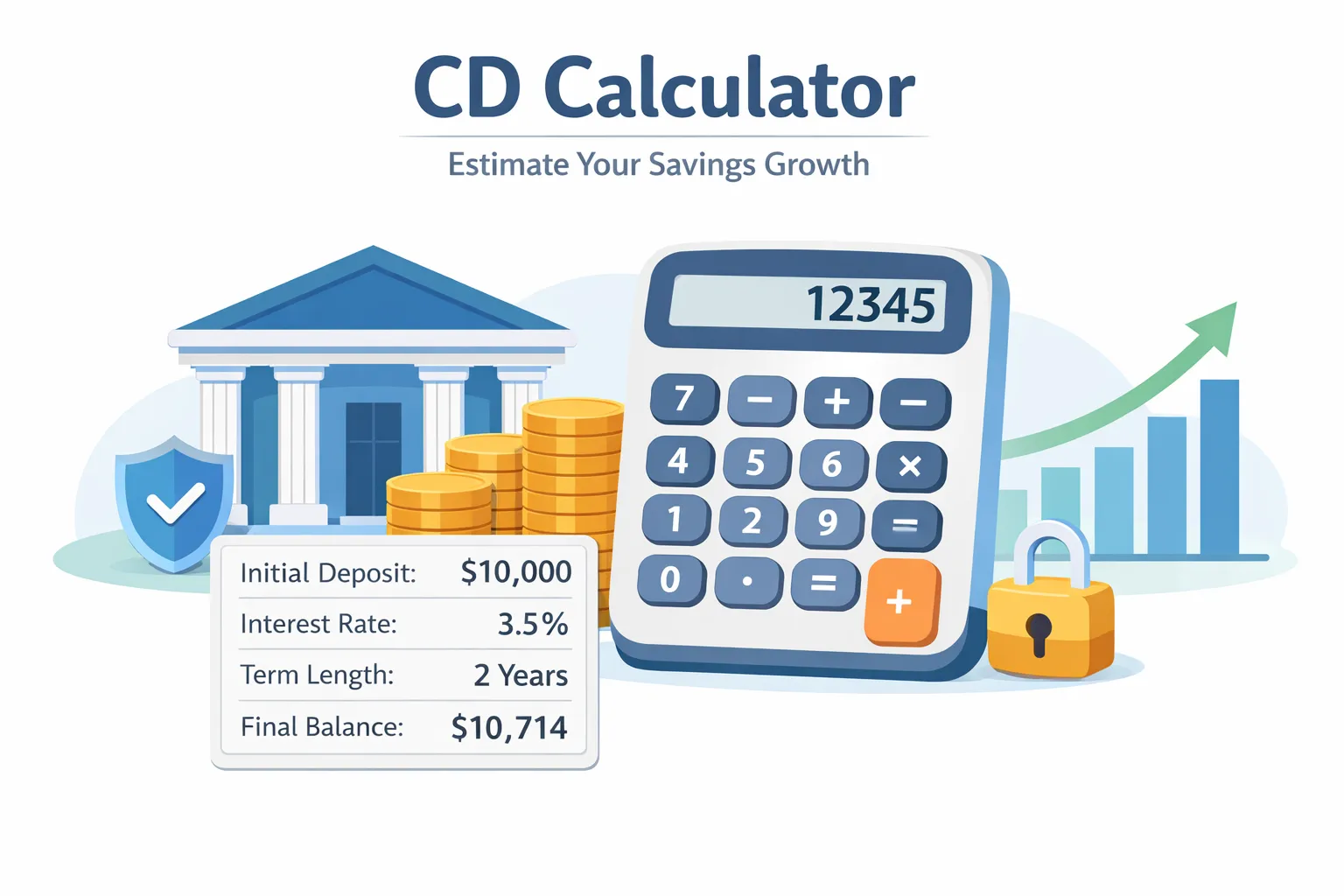

A CD calculator (certificate of deposit calculator) helps you estimate how much your investment will grow over time using fixed interest rates. This free certificate of deposit calculator uses compound interest formulas to provide accurate earnings projections based on your deposit amount, APY (annual percentage yield), term length, and compounding frequency. With over 165,000 monthly searches, it's clear that savers want accurate ways to calculate returns before locking in their money.

This CD interest calculator uses compound interest formulas to show your exact earnings based on your deposit amount, APY (annual percentage yield), term length, and compounding frequency. Whether you're comparing CD rates or planning your savings strategy, this tool provides instant, accurate projections.

Types of CD Calculators

- CD calculator - General purpose calculator for all CD types

- CD interest calculator - Focuses on interest earnings and compound growth

- CD rate calculator - Compares different interest rates and their impact

- CD account calculator - Tracks account growth over time with detailed projections

- CD return calculator - Calculates total return percentage and ROI

- Certificate of deposit calculator - Full-featured tool for comprehensive CD analysis

These tools help you instantly calculate earnings based on your deposit, term, and APY, making it easy to compare options and maximize returns. Whether you're looking for a simple CD interest calculator or a comprehensive certificate of deposit calculator with advanced features, this tool provides everything you need to make informed investment decisions.

How Does a CD Calculator Work?

A CD calculator uses compound interest to determine your final balance. The formula is:

What Each Variable Means

- P = Initial deposit (principal)

- r = Annual interest rate (as decimal)

- n = Compounding frequency per year

- t = Time in years

- A = Final amount

Example: Calculate CD Interest

If you invest $10,000 at 5% APY for 3 years with monthly compounding:

A = 10,000 × (1 + 0.05/12)12×3

A = 10,000 × (1.004167)36

A = 10,000 × 1.1616

A = $11,616

Your CD calculator will show total balance ($11,616) and interest earned ($1,616).

How to Calculate CD Interest Step-by-Step

This directly answers "how to calculate CD interest" and "how do you calculate interest on a CD":

- Enter your deposit amount - The initial principal you'll invest

- Input the interest rate (APY) - The annual percentage yield offered

- Select your CD term - How long you'll keep money invested (months or years)

- Choose compounding frequency - Daily, monthly, quarterly, or annually

- Review your results - See final amount, interest earned, and total return

This CD interest calculator automates all the math, giving you instant results without manual calculations.

How Much Interest Will My CD Earn?

Use this CD earnings calculator to see exactly how much interest your certificate of deposit will generate. The amount depends on four key factors: your initial deposit, the APY (annual percentage yield), the term length, and how often interest compounds. For example, a $10,000 CD at 5% APY for 3 years with monthly compounding will earn approximately $1,616 in interest, giving you a final balance of $11,616.

CD Calculator with Monthly Compounding

Our calculator supports daily, monthly, quarterly, semi-annual, and annual compounding frequencies. Monthly compounding is the most common option offered by banks and credit unions. With monthly compounding, your interest is calculated and added to your principal balance 12 times per year, allowing you to earn interest on your interest more frequently than quarterly or annual compounding. Use the dropdown menu above to compare how different compounding frequencies affect your returns.

CD Interest Rates Today (2026 Update)

Understanding CD interest rates today is crucial before using a calculator. Rates vary significantly based on several factors.

What Influences CD Rates

- Federal interest rate trends - Fed policy directly impacts CD rates

- Inflation - Higher inflation typically means higher CD rates

- Bank competition - Online banks often offer better rates

- Economic conditions - Market stability affects rate offerings

- Term length - Longer terms usually offer higher rates

Typical CD Rate Ranges (2026)

- • Short-term CDs (3-12 months): 4.0% - 5.0% APY

- • Mid-term CDs (1-3 years): 4.5% - 5.5% APY

- • Long-term CDs (5+ years): 5.0% - 6.0% APY

- • Online banks: Often 0.5% - 1.0% higher than traditional banks

Always compare the best CD rates from multiple institutions before investing. Use this CD rates calculator to see how different rates affect your returns.

Best CD Rates & How to Find Them

To maximize returns, always compare the best CD rates available across different institutions. Use this best CD rates calculator 2026 to see how different rates impact your earnings over time.

Where to Find High CD Rates

🏦 Online Banks

Lower overhead means higher rates - often 0.5-1% above traditional banks

🤝 Credit Unions

Member-owned institutions frequently offer competitive rates and lower fees

📊 Comparison Platforms

Financial comparison sites aggregate rates from hundreds of institutions

💼 Brokerage CDs

Available through investment accounts, often with competitive rates

Pro Tip:

Use a CD rates calculator to compare different scenarios before investing. Even a 0.5% rate difference can mean hundreds of dollars over a multi-year term. Explore our other financial calculators to optimize your complete savings strategy.

Factors That Affect Your CD Earnings

Interest Rate (APY)

Higher APY = higher earnings. A 5% APY earns significantly more than 4% over time. On a $10,000 investment for 3 years, the difference between 4% and 5% APY is approximately $300 in additional interest.

Term Length

Longer CDs typically pay more, but lock up your money longer. Consider your liquidity needs before committing to long terms. A 5-year CD might offer 5.5% while a 1-year CD offers 4.5%.

Compounding Frequency

More frequent compounding boosts returns. Daily compounding earns more than monthly, which earns more than annual. For a $10,000 CD at 5% for 3 years:

- Daily compounding: $1,618 interest

- Monthly compounding: $1,616 interest

- Annual compounding: $1,576 interest

Deposit Size

Larger investments generate more interest in absolute dollars. Some banks offer higher rates for larger deposits (jumbo CDs typically start at $100,000).

Strategies to Maximize CD Returns

CD Laddering Strategy

CD laddering involves investing in multiple CDs with different maturity dates. This strategy provides regular access to funds while maintaining higher rates on longer-term CDs. Similar to diversification strategies used in Coast FIRE planning, CD laddering balances liquidity with growth potential.

Example CD Ladder:

- • $5,000 in 1-year CD at 4.5%

- • $5,000 in 2-year CD at 5.0%

- • $5,000 in 3-year CD at 5.5%

- • $5,000 in 5-year CD at 6.0%

As each CD matures, reinvest in a new 5-year CD to maintain the ladder.

Lock in High Rates

Invest when rates peak. If you expect rates to decline, locking in current high rates with longer-term CDs can maximize returns. Monitor Federal Reserve policy for rate trend indicators.

Reinvest Earnings

Compound your gains for long-term growth. When CDs mature, reinvest both principal and interest into new CDs to maximize compound growth over time. If you're planning for early retirement, combine CD laddering with our Coast FIRE calculator to determine when you can stop actively saving and let your investments grow.

CD Calculator vs Savings Account: Which Is Better?

| Feature | CD | Savings Account |

|---|---|---|

| Interest Rate | Fixed (typically higher) ✅ | Variable |

| Flexibility | Low (locked term) | High (withdraw anytime) ✅ |

| Returns | Predictable & guaranteed ✅ | Uncertain (rates change) |

| Early Withdrawal | Penalty applies ⚠️ | No penalty ✅ |

| Best For | Guaranteed returns, planned savings | Emergency funds, flexibility |

CDs are ideal for guaranteed returns when you don't need immediate access to funds, while savings accounts offer flexibility for emergency funds and short-term needs. For homeowners considering other financing options, our HELOC calculator can help you explore home equity lines of credit as an alternative.

Common Mistakes to Avoid

❌ Not Comparing CD Rates

Shopping around can earn you hundreds more. Don't settle for the first rate you see.

❌ Ignoring Early Withdrawal Penalties

Penalties can wipe out months or years of interest. Only invest money you won't need.

❌ Choosing the Wrong Term Length

Match CD terms to your financial goals. Don't lock up emergency funds in long-term CDs.

❌ Forgetting Inflation Impact

If inflation exceeds your CD rate, you're losing purchasing power. Factor in real returns.

Who Should Use a CD Calculator?

👤 Beginners Planning Savings

New to investing? CDs offer predictable, low-risk returns perfect for learning. Check our rent affordability calculator to balance savings with housing costs.

👴 Retirees Seeking Stable Income

Fixed returns provide peace of mind and predictable income streams.

🛡️ Conservative Investors

FDIC-insured up to $250,000 - minimal risk with guaranteed returns.

📊 Anyone Comparing CD Rates

Use this calculator to compare scenarios and find the best CD for your needs.

CD Interest Calculation Formula

CDs use compound interest to calculate your earnings:

- A = P(1 + r/n)^(nt)

- A = Final amount

- P = Principal (initial deposit)

- r = Annual interest rate (as decimal)

- n = Compounding frequency per year

- t = Time in years

Example: Calculate CD Interest

Calculate earnings on a $10,000 CD investment:

How Much Will My CD Earn? (Quick Reference 2026)

Use this table to instantly see how much interest your CD will earn based on deposit size, rate, and term. All figures use monthly compounding.

| Deposit | Rate (APY) | 1 Year | 3 Years | 5 Years |

|---|---|---|---|---|

| $5,000 | 4.5% | +$230 | +$712 | +$1,252 |

| $10,000 | 5.0% | +$511 | +$1,616 | +$2,834 |

| $25,000 | 5.0% | +$1,278 | +$4,040 | +$7,085 |

| $50,000 | 5.5% | +$2,820 | +$9,085 | +$16,162 |

| $100,000 | 5.5% | +$5,641 | +$18,170 | +$32,323 |

Interest earned figures are approximate. Use the calculator above for exact results based on your specific rate and compounding frequency.

CD Calculator by Term: 3-Month to 10-Year

Different CD terms serve different financial goals. Here's how a $10,000 deposit performs across common terms at typical 2026 rates:

Pro Tip: CD Laddering

Split your investment across multiple terms (e.g., $5k each in 1, 2, 3-year CDs). As each matures, reinvest at current rates. This balances liquidity with higher long-term returns.

CD Calculator: Daily vs Monthly vs Annual Compounding

Compounding frequency affects how much you earn. Here's the exact difference on a $10,000 CD at 5% APY for 3 years:

| Compounding | Final Balance | Interest Earned | vs Annual |

|---|---|---|---|

| Daily (365x/year) | $11,618 | $1,618 | +$42 more |

| Monthly (12x/year) | $11,616 | $1,616 | +$40 more |

| Quarterly (4x/year) | $11,608 | $1,608 | +$32 more |

| Annually (1x/year) | $11,576 | $1,576 | baseline |

The difference is small on $10k but grows with larger deposits. On $100,000 at 5% for 5 years, daily vs annual compounding is a $420 difference.

Frequently Asked Questions

How do you calculate CD interest?

Use a CD calculator or compound interest formula with deposit, rate, and term. The formula is A = P(1 + r/n)^(nt), where P is your deposit, r is the annual rate, n is compounding frequency, and t is time in years. This calculator automates the process for accurate results.

What is the best CD calculator?

The best CD calculator includes APY, compounding frequency options, and accurate projections. It should show total earnings, interest earned, and effective return. This calculator provides all these features plus comparison tools to help you maximize returns.

How much can I earn with a CD?

Earnings depend on your deposit, rate, and term length. For example, $10,000 at 5% APY for 3 years with monthly compounding earns approximately $1,616 in interest. Use this calculator to see your exact earnings based on current CD rates.

What are CD interest rates today?

CD interest rates vary based on market conditions and financial institutions. As of 2026, rates typically range from 4-6% APY depending on term length and bank. Online banks often offer higher rates than traditional banks. Always compare rates before investing.

Are CDs better than savings accounts?

CDs offer higher, fixed returns, while savings accounts offer flexibility. CDs are ideal for money you won't need during the term, providing guaranteed returns. Savings accounts are better for emergency funds due to immediate access. Consider your liquidity needs when choosing.

What happens if I withdraw from a CD early?

Early withdrawal typically results in a penalty, often 3-12 months of interest depending on the term. Some banks offer no-penalty CDs with slightly lower rates. Always understand the penalty terms before opening a CD to avoid losing earnings.

How does compounding frequency affect CD returns?

More frequent compounding increases your returns. Daily compounding earns slightly more than monthly, which earns more than annual. For a $10,000 CD at 5% for 3 years: daily compounding earns $1,618, monthly earns $1,616, annually earns $1,576. The difference grows with larger deposits and longer terms.

What is CD laddering?

CD laddering is a strategy where you invest in multiple CDs with different maturity dates. For example, split $15,000 into three $5,000 CDs maturing in 1, 2, and 3 years. This provides regular access to funds while maintaining higher rates on longer-term CDs.

Can I add money to a CD after opening it?

Most traditional CDs don't allow additional deposits after opening. However, some banks offer add-on CDs that permit additional contributions during the term. These typically have slightly lower rates than standard CDs but offer more flexibility.

How do I calculate CD yield?

CD yield (APY) accounts for compound interest. To calculate: APY = (1 + r/n)^n - 1, where r is the annual rate and n is compounding frequency. For example, a 5% rate compounded monthly gives an APY of 5.116%. This calculator shows your effective yield automatically.

What is a 10-year CD calculator used for?

A 10-year CD calculator helps you project long-term savings growth. For example, $25,000 at 5.5% APY for 10 years with monthly compounding grows to approximately $43,000 — earning $18,000 in interest. Long-term CDs lock in rates but offer the highest returns.

How does a CD calculator compounded daily work?

Daily compounding calculates interest every day and adds it to your balance. Using the formula A = P(1 + r/365)^(365×t), a $10,000 CD at 5% for 3 years compounded daily earns $1,618 — about $2 more than monthly compounding. The difference grows significantly with larger deposits.

What is a high-yield CD calculator?

A high-yield CD calculator estimates returns on CDs offering above-average rates, typically 4.5-6%+ APY. Online banks and credit unions often offer these. For example, $20,000 at 5.5% for 2 years earns approximately $2,260 — significantly more than a standard 2% savings account.

How do I calculate CD interest monthly?

Monthly CD interest = (Principal × Annual Rate) ÷ 12. For a $10,000 CD at 5% APY: monthly interest ≈ $41.67. However, with monthly compounding, each month earns slightly more as interest accumulates. After 12 months, total interest is $511 rather than $500 due to compounding.

What is a CD rate of return calculator?

A CD rate of return calculator shows your total return percentage over the investment period. For a $10,000 CD at 5% for 3 years: total return = 16.16% ($1,616 earned). Annualized return = 5.12% (slightly above the stated rate due to monthly compounding).

How much will $10,000 in a CD earn?

At 5% APY for 1 year: ~$511. For 3 years: ~$1,616. For 5 years: ~$2,834. At 4% APY for 1 year: ~$408. For 3 years: ~$1,249. For 5 years: ~$2,167. Use this calculator to see exact earnings for your specific deposit, rate, and term.